This post was written by the former Estonian Credit Union, now Northern Birch Credit Union.

You’ve likely heard about credit scores before (thanks to all those commercials with terrible jingles), but what do you actually know about them? How long have they been around? And what’s the deal with checking them?

A credit score is a number (usually between 300 and 900) that represents your creditworthiness. It’s a standardized measurement that financial institutions and credit card companies use to determine risk level when considering issuing you a loan or a credit card. Basically, it provides a snapshot of how likely you are to repay your debts on time. Widespread use of credit scores has made credit more widely available and less expensive for many consumers.

The FICO score is the best known and most widely used credit score model in North America. It was first introduced in 1989 by FICO, then called Fair, Isaac and Company. It’s also known as the Beacon score in Canada. The FICO model is used by the vast majority of banks and credit grantors, and is based on consumer credit files from the two national credit bureaus: Equifax Canada and TransUnion Canada. Because a consumer’s credit file may contain different information at each of the bureaus, FICO scores can vary, depending on which bureau provides the information to FICO to generate the score.

When credit scores were first introduced, they were used primarily for loaning money. Today, credit scores have much more pull, and that’s why it’s important to understand how they’re calculated. Your monthly car payments, your ability to snag that sweet apartment and even the hiring manager’s decision on that new job you applied for can all be influenced by your credit score

A credit score of 720 or more is considered prime—this means you’re in good shape. Scores under 620 mean you could be turned down for a loan. Scores in the not great (550 to 620) might get you loan approval, but your interest rates will be higher than if you had a prime credit score. Nobody likes the idea of paying more money for no reason, so it makes sense to adopt credit habits that will boost your overall score.

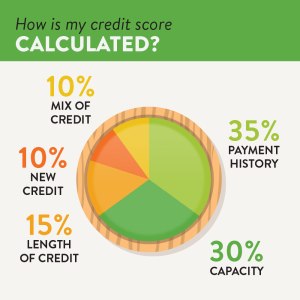

Taking the time to familiarize yourself with how credit scores are calculated is the first step in getting a strong score. Each credit bureau uses a slightly different calculation, but the basic breakdown goes like this:

- 35% is based on payment history. Making payments on time boosts your score.

- 30% is based on capacity. This is one of the areas where the less you use of your total available credit, the better. If you get close to maxing out all your credit cards or lines of credit, it tanks your score, even if you’re making your payments on time.

- 15% is based on length of credit. Good credit habits over a long period of time raise your score.

- 10% is based on new credit. Opening new credit cards (this includes retail credit cards) has a short-term negative effect on your score, so don’t open a whole bunch at once!

- 10% is based on mix of credit. Having a combination of different types of credit (like revolving credit and instalment loans) boosts this part of your score. Credit cards are considered revolving credit, and things like car loans and mortgages are installment loans.

Curious about your credit report? You are entitled to one free credit report per year by mail from Equifax and TransUnion. Spacing out your credit report requests allows you to check on your credit every six months or so. If you can’t wait for a free report by mail, you can always get an instant credit report online from Equifax or TransUnion for approximately $15.

When you receive your credit report, you’ll notice that it does not list your three-digit credit score. Despite this, it’s still a helpful reference because it serves as the basis of your credit score. If you know how a credit score is calculated, then you know how to look for factors on your credit report that might be influencing your score for better or for worse. It’s also an easy way to look at account openings, account closings and what your repayment history looks like.